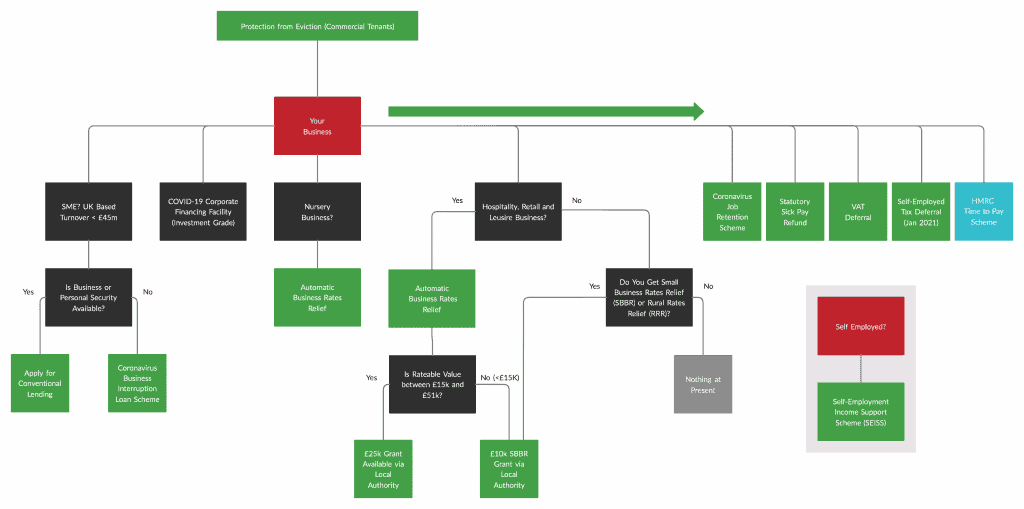

Self-assessment – payments deferral

What we know:

- All taxpayers are now eligible

- For Income Tax Self-Assessment, payments due on the 31 July 2020 may be deferred until 31 January 2021.

- This is an automatic offer with no applications required. No penalties or interest for late payment will be charged if you defer payment until 31 January 2021

- HMRC are extending the filing deadline for 2018-19 tax returns which must be submitted by 23 April 2020

What we are waiting for:

- At this point, we believe that there are no issues requiring HMRC clarification

Care required:

- Interest and surcharges still apply to payments due prior to 31 July 2020

- HMRC will still pursue debts arising prior to 31 July 2020

- Tax returns must still be filed on time

VAT deferral

What we know:

- The deferral will apply to VAT payments normally due between 20 March 2020 until 30 June 2020 – i.e. VAT returns for periods ending 31 March 2020, 30 April 2020 or 31 May 2020

- All UK businesses (VAT registered traders) are eligible

- This is an automatic offer with no applications required. Businesses will not need to make a VAT payment which would normally be due during this period

- Taxpayers will be given until the end of the 2020-21 tax year to pay any liabilities that have accumulated during the deferral period

- VAT refunds and reclaims will be paid by the government as normal

- If you normally pay by direct debit you should cancel the direct debit with your bank if you are unable to pay. Please do so in sufficient time so that HMRC do not attempt to automatically collect the VAT on receipt of your VAT return

- The deferral will not be treated as a default for VAT penalty purposes

What we are waiting for:

- At this point, we believe that there are no issues requiring HMRC clarification

Care required:

- If you have a Direct Debit set up, this should be cancelled urgently otherwise HMRC may still attempt to collect the VAT

Statutory sick pay

What we know:

- You are eligible for the scheme if:

- your business is UK based; and

- your business is an SME and employs fewer than 250 employees as of 28 February 2020

- the refund will cover up to 2 weeks’ Statutory Sick Pay (“SSP”) per eligible employee who has been off work because of COVID-19

- employers will be able to reclaim expenditure for any employee who has claimed SSP (according to the new eligibility criteria) as a result of COVID-19

- employers should maintain records of staff absences and payments of SSP, but employees will not need to provide a GP fit note. If evidence is required by an employer, those with symptoms of coronavirus can get an isolation note from NHS 111 online and those who live with someone that has symptoms can get a note from the NHS website

What we are waiting for:

- the eligible period for the scheme will commence the day after the regulations on the extension of SSP to those staying at home comes into force (date not yet known)

- the government will work with employers over the coming months to set up the repayment mechanism for employers as soon as possible

Care required:

- you will need appropriate evidence of sickness to support your claim

Job retention

What we know:

- Employment Law must be considered carefully when furloughing employees – employees are entitled to be paid in accordance with their contract and therefore there is no automatic entitlement to reduce an employee’s pay

There is a lot of detail in the guidance – below is a summary of some of the key points (Government source)

Organisations – qualifying conditions

- Any UK organisation can apply for the grant (including businesses, charities, recruitment agencies, public authorities, companies in Administration)

- You must have created and started a PAYE payroll scheme on or before 28 February 2020 and have a UK bank account

- To be eligible for the subsidy employers should write to their employee confirming that they have been furloughed and keep a record of this communication

Employees you can claim for

- Employee-shareholders will be eligible for the scheme, but only in respect of their salary

- Employees hired after 28 February 2020 cannot be furloughed or claimed for in accordance with this scheme

- Furloughed employees must have been on your PAYE payroll on 28 February 2020, and can be on any type of contract (including full-time employees, part-time employees, employees on agency contracts, employees on flexible or zero-hour contracts)

- The scheme also covers employees who were made redundant since 28 February 2020, if they are rehired by their employer

- You do not need to place all your employees on furlough. However, those employees who you do place on furlough cannot undertake work for you

- Employees must be on furlough for a minimum of three weeks in order to be eligible to be included in the grant claim

- There are additional rules for:

- Employees on unpaid leave

- Employees on sick leave

- Employees with more than one job

- Employees undertaking volunteering or training

- Employees on maternity leave or similar leave

- The National Living Wage and National Minimum Wage does not apply to furloughed employees

How much you can claim

- You will receive a grant from HMRC to cover:

- the lower of:

- 80% of an employee’s regular wage; or

- £2,500 per month

- PLUS the associated:

- employer National Insurance contributions; and

- minimum automatic enrolment employer pension contributions on that subsidised wage

- the lower of:

- Regular wage is defined as:

- for full-time and part-time salaried employees, the employee’s actual salary before tax, as of 28 February 2020 should be used to calculate the 80%. Fees, commission and bonuses should not be included

- for employees whose pay varies, there are separate rules

Not covered by the grant

- The following amounts are not included in the claim:

- any amount you may voluntarily choose top-up salary in addition to the grant

- employer National Insurance Contributions on any top-up

- automatic enrolment contributions on any top-up salary

- voluntary automatic enrolment contributions above the minimum mandatory employer contribution of 3% of income above the lower limit of qualifying earnings

Claiming

- You can only submit one claim at least every 3 weeks, which is the minimum length an employee can be furloughed for. Claims can be backdated until the 1 March if applicable

- You must utilise all of the grant you receive in respect of an employee to pay their gross pay. No fees can be charged from the money that is granted. You can choose to top up the employee’s salary, but you do not have to

- There is various information required as part of the claim – see the guidance

- You will need to calculate the amount you are claiming

- HMRC will retain the right to retrospectively audit all aspects of your claim.

Other

- The grant is taxable income for the purposes of income and corporation tax [the wages/furlough payments are allowable deductions]

What we are waiting for:

- HMRC are working to set up the online portal system for reimbursement which will pay funds electronically to claimants. Existing systems are not set up to facilitate payments to employers

- It is not currently clear:

- whether a furloughed employee may return to work and be furloughed again at a later date and, if so, how long before they can be ‘re-furloughed’ and how often (remembering that an employee’s furlough must be three weeks for their wages to be eligible for inclusion in the grant claim)

- whether, under Company Law, all directors may be furloughed as Company Law may require a minimum of one active director; and if so

- whether HMRC will deem one director or a sole director to be active and therefore not eligible to be furloughed

- Specifically, relating to the above, it is not clear for directors whether:

- a director may carry on the ‘statutory duties’ if furloughed

- what activities HMRC will accept as falling within or outside of ‘statutory duties’ (e.g. payroll, VAT returns, other tax returns, paying suppliers etc may all be deemed to be ‘work’ rather than statutory duties)

Care required:

- changing the status of employees remains subject to existing Employment Law and, depending on the employment contract, may be subject to negotiation

- you should take appropriate Employment Law advice to ensure that employees are treated fairly and are not discriminated against

Business interruption loans

What we know:

- Further details are being published 26 March 2020

- The temporary Coronavirus Business Interruption Loan Scheme supports SMEs with access to loans, overdrafts, invoice finance and asset finance of up to £5 million and for up to 6 years

- You will need a Business Plan

- SMEs qualify if their turnover is under £45m, and they meet the other eligibility criteria – click here

- The government will also make a Business Interruption Payment to cover the first 12 months of interest payments and any lender-levied fees, so smaller businesses will benefit from no upfront costs and lower initial repayments

- The government will provide lenders with a guarantee of 80% on each loan (subject to pre-lender cap on claims) to give lenders further confidence in continuing to provide finance to SMEs. The scheme will be delivered through commercial lenders, backed by the government-owned British Business Bank

- There are 40 accredited lenders able to offer the scheme, including all the major banks

What we are waiting for:

- It is not clear:

- what appetite the banks actually have for this lending

- what risk loading they will apply to the rates of interest

- what due diligence they will undertake on the Business Plan

Care required:

- You may be required to provide security and/or personal guarantees for the entire loan not just the 20%

- The 80% guarantee is only likely to apply if the lender cannot ultimately recover the whole of the loan from you

- If you are providing security and/or personal guarantees, you should take legal advice on the implications of this

- You will need to consider how any such security and/or personal guarantees interact with any other borrowings and security you have with the same lender

Self employed & partnerships

What we know:

- A grant is available of up to 80% of average monthly profits, with the grant capped at £2,500

- To be eligible for the grant you must:

- have submitted your Income Tax Self-Assessment tax return for the tax year 2018-19

- traded in the tax year 2019-20

- be trading when you apply, or would be except for COVID-19

- intend to continue to trade in the tax year 2020-21

- have lost trading/partnership trading profits due to COVID-19

- Your self-employed trading profits must also be less than £50,000 and more than half of your income come from self-employment. This is determined by at least one of the following conditions being true:

- having trading profits/partnership trading profits in 2018-19 of less than £50,000 and these profits constitute more than half of your total taxable income

- having average trading profits in 2016-17, 2017-18, and 2018-19 of less than £50,000 and these profits constitute more than half of your average taxable income in the same period

- The grant will run for an initial three month period payable as a lump sum, targeted for the start of June 2020

- HMRC will contact eligible individuals to make a claim via an online form – they are asking that you do not contact HMRC as HMRC will be automatically instigating claims

- HMRC are extending the filing deadline for 2018-19 tax returns which must be submitted by 23 April 2020

- The self-employed and partners in partnerships will have access to:

- Business Interruption Loans

- Universal Credits to support a drop in income

- Hardship Grants

What we are waiting for:

- Full details of how the scheme will operate

- How the other income and averaging calculation will work if, in the three year period:

- there have been trading losses incurred

- there has been other loss relief or other tax relief claimed

- there have been capital gains

- other income exceeds 50% for only part of the relevant periods

- How any clawback will be calculated

Care required:

- Being able to repay in the future, cash flow.

Corporation tax

What we know:

- There is currently no specific relief for corporation tax payments

Companies

Three-month extension to company accounts filing deadline

What we know:

- Companies will have to apply for the 3-month extension to be granted (click here)

- Those citing issues around COVID-19 will be automatically and immediately granted an extension

- Applications can be made through a fast-tracked online system which will take just 15 minutes to complete

What we are waiting for:

- Details of how to access the online system

- Guidance on the definition of “citing issues around COVID-19”

Care required:

Filing accounts late can adversely impact a company. You should consider, for instance:

- The impact on the company’s credit rating

- Whether late filing would cause a breach of any banking or loan facilities

- Whether late filing would cause a breach of any other agreements or covenants

Relaxation of insolvency laws

What we know:

- The government has announced the following:

“The new legislation will implement these plans, including a short moratorium or ‘breathing space’ that will give companies in difficulty time to explore options for rescue.

Current insolvency rules stipulate that directors of limited liability companies can become personally liable for business debts if they continue to trade when uncertain about whether their businesses can continue to meet their debts. Relaxation of these wrongful trading rules will reassure directors that the difficult decisions they have to make about the future viability of their business will not have to be unduly influenced by the exceptional circumstances which are entirely beyond their control.”

What we are waiting for:

- The legislation is not yet enacted and therefore we do not have absolute certainty as to the technical content

Care required:

- The insolvency rules are complex and we always strongly recommend that clients seek professional advice if they are either anticipating or actually experiencing financial difficulty.

Director and Shareholder Meetings

What we know:

- Company Law and the Memorandum & Articles of Association set out the procedures for meetings

- In these uncertain times, it will be increasingly important that Directors hold regular meetings and draw up minutes of those meetings to evidence the decisions made

- In light of the current restrictions on movements, meetings may need to be held by phone or video conference. In such cases, we strongly recommend that:

- the minutes record where/how an individual attended the meeting

- the minutes are circulated and agreed together with copies of any formal resolutions voted upon

What we are waiting for:

- It is not clear whether participation in such meetings will be deemed to be “work” for the purposes of furloughing directors (see section 4)

Care required:

- If you are concerned regarding Company Law issues around holding remote access meetings, we recommend that you contact a Company Law specialist

Insurance

What we know:

- Many clients will carry business insurance policies which may include cover for business interruption

- Often the policies will contain wording regarding Force Majeure covering epidemics, pandemics and similar disruptions

Care required:

- Your policy may require you to immediately notify your insurer of circumstances that might lead to a claim. You should check your policy carefully and contact your insurer if necessary.

HMRC business and self-employment helpline 0800 024 1222

Resources:

- 2. Briefing Note – HMRC Support for Businesses (Summary)

- 3. Briefing Note – HMRC Support for Self-Employed (Summary)

- 4. Briefing Note – Support Negotiating Time to Pay with HMRC

- 5. Briefing Note – How to Manage Your Relationship with HMRC (Basic Rules)

- 6. Factsheet – Furloughed Workers (FAQs)

- 7. Factsheet – Business Interruption Loan Scheme (Eligibility, How it Works and Find a Lender)

- 8. How to Improve Working Capital Through Tax Reliefs

For more information, feel free to contact Matt Bryant <matt.bryant@zigzagca.com>